February 1, 2023

Guardian: Round-up of 2022 and what 2023 may hold

Blog by Sam Davis, Head of Distribution Strategy, Guardian

What a year 2022 was. So much has happened, and little of it happy news. We know clients need us all more than ever – and by us, I mean the whole industry. Providers and advisers have spent the year supporting our clients through a time of turbulence and uncertainty, doing what we do best. Which is offering them protection that won’t let them down and looking to help improve their financial resilience.

Let’s have a quick look back at what we did last year. At the start of Q1, we were approaching the end of our second year of living with the pandemic. This ongoing sense of uncertainty was compounded in February with Russia’s invasion of the Ukraine; war undermining our sense of peace and stability. However, in times of unease, people need certainty, and they need us to keep doing what we do well.

At Guardian, Q1 saw us promote the recent launch of our newest HALO claims support partner, Krysalis Consultancy. We were delighted to be the first protection brand to partner with Krysalis and play our part in bringing such an important, life-changing service to the industry. You may have seen our Head of Claims, Phil Deacon, in the press. Or you may have tuned in to one of our 4 HALO mini-series of podcasts on our website, featuring our support partners talking about how much they do to help clients when they need us most.

Then came Q2, and another challenge was beginning to bite: the cost of living. The impact of the Russia-Ukraine war on energy prices, combined with the economic aftermath of the pandemic and impacts of Brexit, all resulted in rising prices. Around us we were seeing inflation rising, approaching double digits for the first time since 1982.

There was talk of how the inflationary pressure was going to affect clients, and our Actuarial Director, Nischal Singh, shared his thoughts in an article for Health and Protection magazine. In the face of rising prices, we wanted to help advisers continue to have good protection conversations. At the time, over 71% of advisers[1] said they had at least some clients who were cutting back on spending as a result of the cost-of-living crisis. We ran a webinar called ‘talking protection in a cost crisis’ with Cover magazine. What became extremely clear during this webinar debate was that, during inflationary times, the need for protection is amplified.

Alongside dealing with the cost-of-living challenge, we wanted to help advisers to continue to have high-quality protection conversations about critical illness cover. With this in mind, we did some research with Protection Guru to test the quality of our critical illness definitions. Protection Guru ran some analysis on the ‘Big Four’ most claimed-for critical illness conditions, which are cancer, heart attack, stroke, and multiple sclerosis. And by using extensive incidence data, a panel of independent medical experts gave providers’ critical illness definitions a score of 0-100% based on how likely it is that a claim will be paid. Only Guardian scored 100% across the 4 most claimed for critical illness conditions. So, we launched our Big Four campaign, helping show the differences in quality of definitions around the most claimed-for critical illness conditions to better support advisers in clearly explaining these differences to clients.

You can’t look back at 2022 without talking about Consumer Duty. The new guidance, published in July, represents a shift in focus from the previous TCF outcomes. It introduces a new Consumer Principle that requires firms to act to deliver good outcomes for its retail customers.

[1] Guardian survey to 701 advisers, between 11 August and 3 September 2022.

In early Q3, we upgraded our quote and apply system – Protection Builder 2.0 – to make it easier for advisers to bring their advice to life. To design the upgrade, we worked with a team of advisers, seeking their insight to create an even simpler, more flexible digital experience that reflects how advisers want to work with their clients in this evolving digital age.

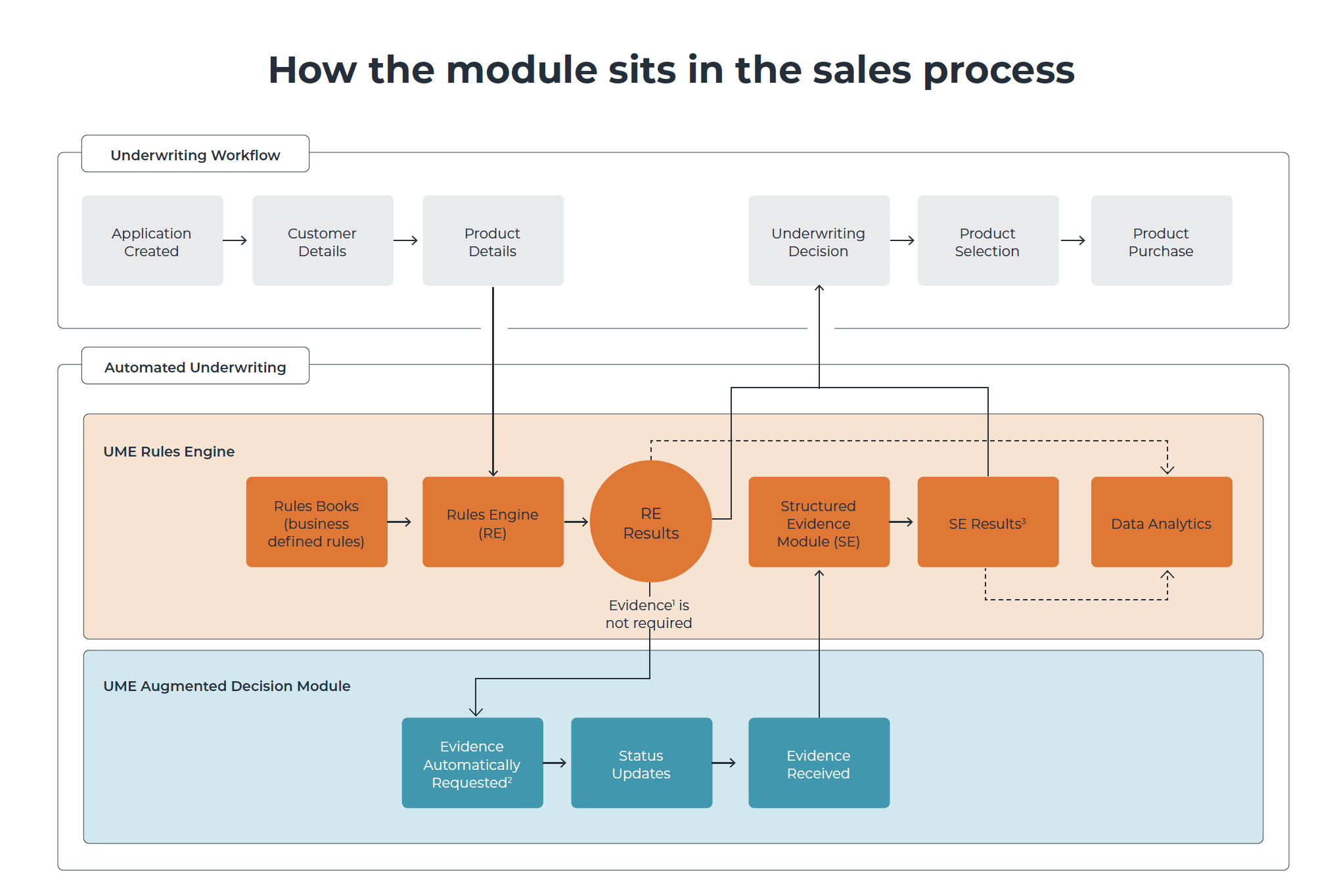

We also upgraded our Underwriting Qi tool to give more accurate pre-sales decisions at the touch of a button. The upgrade allows advisers to enter key disclosures upfront – including multiple conditions, smoker status, family history, medical history, job, overseas travel, sports and pastimes, as well as alcohol usage – to give an immediate indication of any rating which will affect the client’s premium.

At the same time, we announced changes to our underwriting question-set for mental health. This was designed to help support full disclosure, while making it easier and faster for clients with these conditions to get a decision and be offered appropriate terms. We introduced clearer mental health questions, with conditions separated out in line with ABI guidelines, differentiating between anxiety, depression, self-harm and suicidal thoughts. We also made enhancements for asthma, diabetes, hypertension and cholesterol, with fewer evidence needed for some conditions.

Moving into the most recent quarter – well, we all know what happened at the end of last year! It’s been a time of significant political upheaval and severe economic consequences, all of which have had a dramatic impact on our industry. Not least the mortgage market. It’s been, quite frankly, a rollercoaster from one week to the next. At Guardian, to help advisers deal with this environment, we published the results of some research amongst 700 advisers to provide a clearer view of what they were experiencing when it comes to protection. We found that, despite the pressures (and maybe even because of them), 62%[2] felt there was still a raised appetite to talk about protection. While times are tough for many people, they still want the certainty that protection can provide.

Looking into 2023, most experts predict we’re entering a period of prolonged recession. What people will need most is help with their finances. Advisers are well positioned to do this, and I expect to see the industry move to help people meet their protection needs in a way that gives them financial resilience and meets their budgets. As our Sales Director said recently at an industry conference, it’s a time for our industry to keep calm and keep doing what we do best: help customers.

2023 is also the year we’ll implement Consumer Duty. From an advice perspective, I expect to see a move towards placing greater emphasis on protection during the fact-find – establishing a client’s financial resilience so they can clearly identify their protection need and address it. I expect to see a move towards better, clearer literature and support, as well as increased use of a menu approach where clients can pick and mix what they need to maximise the effectiveness of their budgets.

Overall, despite the obvious economic challenges, I think it’s going to be a good year for protection as people seek to put themselves in the best position possible to deal with life’s undeniable uncertainty.

[2] Guardian survey to 701 advisers, between 11 August and 3 September 2022.

Guardian Financial Services is an appointed representative of Scottish Friendly Assurance Society Limited. All products are provided by Scottish Friendly.